Are Home Loan Presumptions a Bargain?. Home loan Professor. Cortesi GR. (2003 ). Mastering Property Principals. p. 371 Residences: Slow-market savings the 'buy-down'. CNN Cash. http://www.unece.org/hlm/prgm/hmm/hsg_finance/publications/housing.finance.system.pdf, p. 46 Renuart E. (2012 ). Property Title Difficulty in Non-Judicial Foreclosure States: The Ibanez Time Bomb?. Albany Law School Single-family notes. Fannie Mae. Security Instruments.

" About CMHC - CMHC". CMHC. " Comparing Canada and U.S. Real Estate Financing Systems - CMHC". CMHC. Crawford, Allan. " The Residential Home Mortgage Market in Canada: A Primer" (PDF). bankofcanada.ca. " Brand-new home mortgage guidelines push CMHC to embrace insurance coverage basics". 14 April 2014. " New home mortgage stress test rules begin today". CBC News. Recovered 18 March 2019.

Government of Canada. Evans, Pete (July 19, 2019). " Mortgage stress test guidelines get more lax for first time". CBC News. Retrieved October 30, 2019. Zochodne, Geoff (June 11, 2019). reverse mortgages how they work. " Regulator safeguards home mortgage tension test in face of push-back from industry". http://rylanippy116.tearosediner.net/h1-style-clear-both-id-content-section-0-the-single-strategy-to-use-for-how-to-taxes-work-on-mortgages-h1 Financial Post. Obtained October 30, 2019. " Financing minister Expense Morneau to examine and consider changes to mortgage tension test".

Little Known Facts About How Do Buy To Let Mortgages Work Uk.

Congressional Spending Plan Office (2010 ). p. 49. International Monetary Fund (2004 ). pp. 8183. ISBN 978-1-58906-406-5. " Best fixed rate home loans: two, three, five and 10 years". The Telegraph. 26 February 2014. Recovered 10 May 2014. " Need for fixed mortgages strikes all-time high". The Telegraph. 17 May 2013. Obtained 10 May 2014. United Nations (2009 ).

p. 42. ISBN 978-92-1-117007-8. Vina, Gonzalo. " U.K. Scraps FSA in Most Significant Bank Guideline Overhaul Considering That 1997". Businessweek. Bloomberg L.P. Retrieved 10 May 2014. " Regulatory Reform Background". FSA website. FSA. Retrieved 10 May 2014. " Financial Solutions Bill gets Royal Assent". HM Treasury. 19 December 2012. Recovered 10 May 2014. " Covered Bond Outstanding 2007".

www.unece.org. owner, name of the document. " FDIC: Press Releases - PR-60-2008 7/15/2008". www.fdic.gov. (PDF). Soros, George (10 October 2008). " Denmark Uses a Model Home Mortgage Market" through www.wsj.com. " SDLTM28400 - Stamp Duty Land Tax Manual - HMRC internal handbook - GOV.UK". www.hmrc.gov.uk.

Top Guidelines Of How Do First And Second Mortgages Work

A home mortgage is a type of loan that is protected by property. When you get a home mortgage, your loan provider takes a lien against your property, indicating that they can take the property if you default on your loan. Mortgages are the most common type of loan used to purchase genuine estateespecially home.

As long as the loan amount is less than the value of your property, your lender's danger is low. Even if you default, they can foreclose and get their money back. A home mortgage is a lot like other loans: a loan provider provides a debtor a specific amount of cash for a set amount of time, and it's paid back with interest.

This means that the loan is secured by the property, so the lender gets a lien versus it and can foreclose if you fail to make your payments. how do mortgages work. Every home loan comes with certain terms that you should understand: This is the quantity of cash you borrow from your loan provider. Generally, the loan amount has to do with 75% to 95% of the purchase cost of your home, depending upon the kind of loan you utilize.

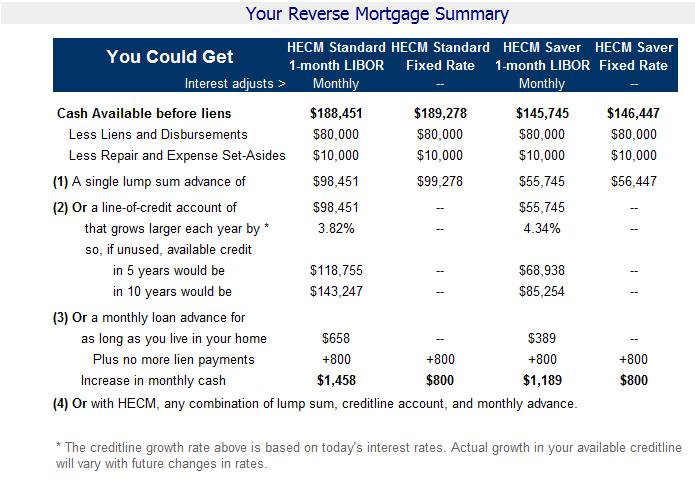

More About How Do Reverse Mortgages Work?

The most common home mortgage loan terms are 15 or thirty years. This is the process by which you pay off your home loan in time and consists of both primary and interest payments. In many cases, loans are totally amortized, meaning the loan will be completely settled by the end of the term.

The interest rate is the expense you pay to obtain cash. For home mortgages, rates are usually between 3% and 8%, with the very best rates available for mortgage to debtors with a credit report of a minimum of 740. Home loan points are the charges you pay in advance in exchange for reducing the interest rate on your loan.

Not all home mortgages charge points, so it is very important to inspect your loan terms. The variety of payments that you make per year (12 is normal) impacts the size of your regular monthly home mortgage payment. When a lender approves you for a house loan, the home loan is set up to be paid off over a set duration of time.

The Facts About What Can Itin Numbers Work For Home Mortgages In California Revealed

Sometimes, lenders might charge prepayment penalties for paying back a loan early, but such charges are unusual for a lot of mortgage. When you make your monthly home loan payment, every one appears like a single payment made to a single recipient. However home mortgage payments really are burglarized numerous various parts Additional reading - how does chapter 13 work with mortgages.

Just how much of each payment is for principal or interest is based on a loan's amortization. This is a calculation that is based on the quantity you obtain, the regard to your loan, the balance at the end of the loan and your rate of interest. Home mortgage principal is another term for the amount of money you obtained.

Oftentimes, these costs are contributed to your loan amount and paid off gradually. When referring to your home loan payment, the principal quantity of your home loan payment is the portion that breaks your outstanding balance. If you obtain $200,000 on a 30-year term to buy a house, your regular monthly principal and interest payments may be about $950.

6 Simple Techniques For Explain How Mortgages Work

Your total regular monthly payment will likely be greater, as you'll also need to pay taxes and insurance coverage. The rate of interest on a mortgage is the quantity you're charged for the cash you obtained. Part of every payment that you make goes toward interest that accumulates between payments. While interest cost becomes part of the cost constructed into a home mortgage, this part of your payment is generally tax-deductible, unlike the principal part.

These may consist of: If you choose to make more than your scheduled payment monthly, this amount will be charged at the exact same time as your typical payment and go directly toward your loan balance. Depending on your loan provider and the type of loan you use, your lending institution may require you to pay a portion of your real estate taxes monthly.

Like property tax, this will depend upon the loan provider you utilize. Any amount collected to cover property owners insurance will be escrowed till premiums are due. If your loan amount surpasses 80% of your residential or commercial property's worth on a lot of traditional loans, you may have to pay PMI, orprivate home loan insurance coverage, monthly.

The smart Trick of How Mortgages Work In Monopoly That Nobody is Talking About

While your payment might include any or all of these things, your payment will not usually include any charges for a homeowners association, condominium association or other association that your residential or commercial property is part of. You'll be required to make a different payment if you come from any property association. Just how much home mortgage you can afford is usually based upon your debt-to-income (DTI) ratio.